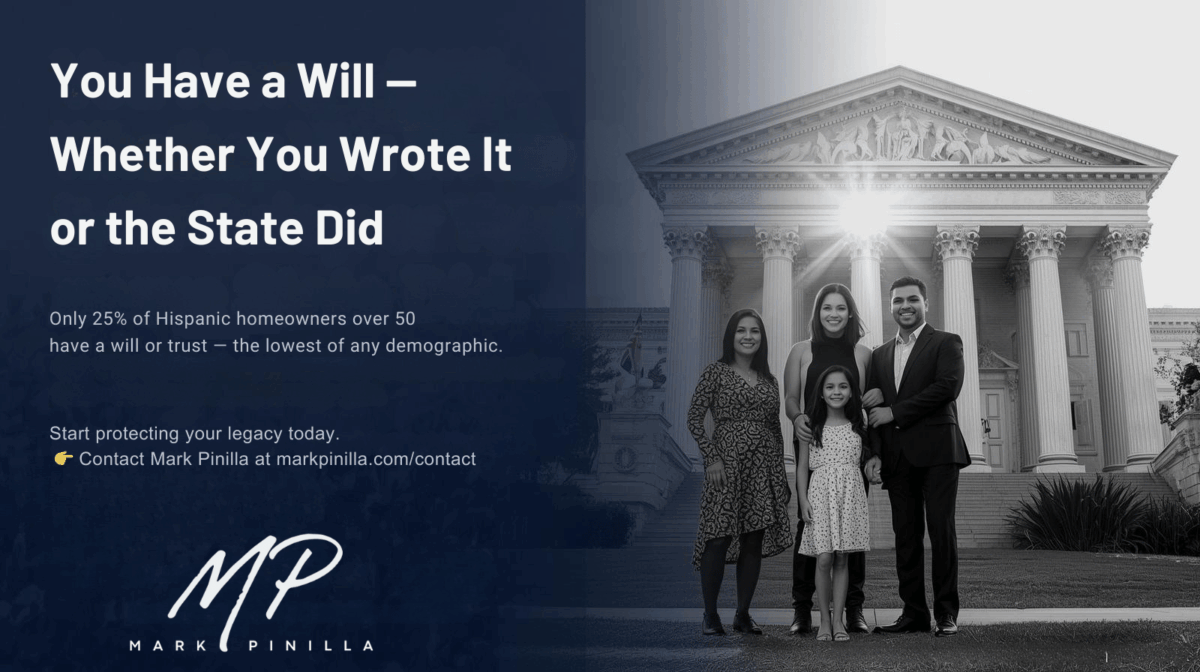

Only 25% of Hispanic homeowners over age 50 have a will or trust — the lowest rate of any demographic in the U.S.

This isn’t just a stat. It’s a red flag for unprotected generational wealth.

Because when you don’t have an estate plan, the state decides: 🏠 Who gets your home 👨👩👧 Who raises your children 💰 How your assets are divided ⏳ How long your family waits 💔 And how much it costs them in probate

If you don’t have a will, the state has one for you. But it won’t reflect your values, protect your legacy, or preserve peace in your family.

And while estate planning is often misunderstood as a “luxury,” it’s actually the foundation of wealth preservation. Especially if you’re a homeowner, a parent, or a business owner.

Here’s what you need to protect your assets:

✅ A Living Will – outlines your healthcare decisions ✅ A Revocable Trust – avoids probate, keeps your affairs private ✅ A Durable Power of Attorney – gives a trusted person legal authority if needed ✅ A valid Will – ensures your wishes are clear and enforceable

🎥 Watch this quick video to see how easy it is to begin:

📩 Ready to protect what matters most?

Contact Mark Pinilla to learn how you can start protecting your assets today.

I’ll show you how to start the process.

💬 Because estate planning isn’t optional. It’s essential for any family building a legacy.

For too long, we’ve been taught that success is something you show. However, real wealth is built not flaunted, and that truth is finally taking root in our community.

Because of this shift, Latino families are no longer chasing image alone. Instead, we are choosing freedom, legacy, and long-term control over short-term applause.

Why Flash Fails and Freedom Wins

Let’s be honest.

Flash is temporary. Flex fades. However, freedom compounds.

When we define wealth by what we show, we get trapped in survival mode. As a result, we stay busy but never build ownership.

Instead, we must define wealth by what we own, invest in, and protect. For this reason, Latino families are making powerful shifts:

Less showing off, more showing up

Fewer liabilities, more income-generating assets

No more chasing approval – only chasing freedom

Más Que Dinero: My Philosophy for Latino Wealth

Más Que Dinero is not just a phrase — it’s my philosophy.

I created this philosophy through deep reflection and collaboration with organizations like NAHREP and the Hispanic Wealth Project, both of which have shaped how I see wealth, legacy, and purpose in the Latino community.

To me, Más Que Dinero means that true wealth goes beyond income. It’s about building a life of purpose, ownership, and legacy.

This philosophy is rooted in five guiding beliefs:

Value time over status

Build assets, not just income

Live below your means so you can rise above limits

Invest with intention, not impulse

Define wealth by what you leave behind, not what you show

This is more than financial advice. It’s a personal mission. It’s a cultural reset. It’s a mindset that empowers Latino professionals and immigrant parents to shift from survival mode to strategic growth.

Más Que Dinero is still new, but the values it reflects have been in our families for generations — sacrifice, discipline, faith, and hard work.

Why Real Wealth Is Built Not Flaunted

The 2025 State of Hispanic Wealth Report confirms that Latino families are not just dreaming about wealth — they are actively building it. Across the four pillars of prosperity, the data tells a story of cultural transformation:

Homeownership: Hispanic homeownership reached 49.5%, holding steady despite rising interest rates and housing costs. It reflects resilience and the desire for permanence and generational equity.

Entrepreneurship: Latinos started 36% of all new businesses in the U.S., nearly double our share of the population. The challenge now is scaling beyond solopreneurship and building long-term equity through systems and teams.

Investments: Our participation in retirement and financial markets is growing, but still below national averages. The report highlights a rising awareness of long-term investing through culturally relevant education and access.

Asset Protection: The report reveals a critical gap — very little data is available on the use of trusts, wills, life insurance, or estate planning in Latino communities. This silence speaks volumes. Protecting what we build is just as important as building it. We must normalize conversations around legal tools that safeguard our legacy.

This is not just data. It’s a reflection of shifting priorities — from spending to strategy, from income to ownership. The Más Que Dinero philosophy aligns with this momentum and gives it structure, language, and urgency.

What Real Wealth Looks Like in Real Life

Real wealth is quiet. It does not beg to be seen.

It shows up in:

A paid-off home

Monthly income from dividend stocks or rental units

Emergency funds that eliminate fear

Trusts and wills that secure your family’s future

Real wealth isn’t loud. It’s strong, steady, and unstoppable. Therefore, we must prioritize building it every day.

How to Start Your Shift Right Now

You don’t need six figures to start building wealth. You only need the courage to take one step.

Here are three ways to begin today:

Audit your spending. What are you buying to impress others?

Start investing. Open a simple brokerage account and buy a low-cost index fund.

Adopt the Más Que Dinero mindset. Choose actions that create freedom, not just applause.

Every decision matters. Every dollar is a tool. Every habit is a seed.

Build What They Cannot Take Away

If you’re a Latino professional or immigrant parent, you are not just working to survive. You are building something bigger.

You were not born to hustle endlessly and leave nothing behind. You were born to build. To own. To change your family tree.

Start now:

Embrace the Más Que Dinero philosophy

Talk to your children about assets, not just jobs

Invest in freedom, not flex

Because real wealth is built not flaunted. And what you build today becomes someone else’s freedom tomorrow.

✉️ Ready to Build Your Legacy? Contact Me

If you’re ready to stop showing wealth and start building it — for your children, your future, and your freedom — let’s connect.

I’ll help you:

Apply the Más Que Dinero philosophy to your own life

Create a practical wealth-building strategy

Shift your mindset from consumer to creator

📩 Contact Me Take the first step toward legacy. Because the time is now.

Mark Pinilla at NAHREP Fort Lauderdale’s “Level Up 2026: Strategies for Success”

Mark Pinilla delivered a powerful and timely presentation titled “Fortifying the Latino Brand and Leveraging Your NAHREP Membership” at NAHREP Fort Lauderdale’s signature event, Level Up 2026: Strategies for Success.

His keynote was a compelling call to action for all real estate professionals to become the bridge that helps build the perfect Latino family—one that:

Owns a home

Owns a business

Invests in the market

Protects what they’ve worked hard for

Mark emphasized that NAHREP members must:

Connect with like-minded individuals to drive collective success

Educate themselves and their communities to create long-term wealth

Build and serve their local communities with purpose

Live out the NAHREP 10 Disciplines as role models for generational change

This session wasn’t just informational—it was transformational, urging Latino professionals to step into leadership, legacy, and significance.

👉 Follow the links below to learn more, get involved, and explore resources that will help you build your legacy.

Redefine wealth to build lasting prosperity. That’s the shift Latino families and professionals must make if we’re serious about changing our financial reality. This isn’t about working harder. It’s about thinking differently.

Many of us were raised to believe that wealth is something you show. Cars, clothes, and brand names become symbols of success. But those symbols come with invisible costs: debt, stress, and missed opportunities for real ownership.

Discipline #1 from the NAHREP 10 is clear. We must move beyond the surface and develop a mature understanding of wealth. True prosperity doesn’t shout. It compounds.

The Flash Trap

Carlos was a top real estate agent. Designer clothes, expensive car, no investments. His sister Mariana lived modestly but bought her first property at 28. Ten years later, Carlos was juggling debt. Mariana had multiple streams of income.

Same family. Same opportunity. Different mindset.

Too often, we trade long-term security for short-term status. We can’t build a financial legacy on image alone. We have to redefine wealth to build lasting prosperity and we have to start now.

What Real Wealth Looks Like

Real wealth gives you options. It includes:

Income-producing assets

Financial stability over flash

Room to take risks without panic

Legacy for the next generation

This kind of wealth isn’t loud or visible. It’s intentional, disciplined, and rooted in clarity.

Consumption vs. Control

Many spending habits come from a need for recognition. But when you shift from spending to investing, you stop seeking validation and start building power.

Ask yourself:

Is this purchase for impact or image?

Will this decision move me closer to freedom?

Am I acting from strategy or emotion?

The more you ask these questions, the faster you gain control of your financial story.

The State of Latino Wealth

According to the Federal Reserve Survey of Consumer Finances, only 33 percent of Latinos own a retirement account, and just 15 percent own a brokerage account. That means the vast majority are not participating in the long-term wealth-building tools that drive financial freedom.

These are not just numbers. They are red flags.

When 96 percent of Latinos have transactional accounts, but only a fraction invest, it shows that most are stuck in a cycle of spending and saving — not growing.

This isn’t just a gap in numbers. It’s a gap in access, education, and mindset.

The system wasn’t designed with Latino stories in mind. But we don’t need permission to change that. We need tools, mentors, and a shift in perspective. We must move from chasing status to creating security.

This is why the NAHREP 10 Certified Trainer Program was created. It exists to spread culturally relevant financial education, increase Latino homeownership, and expand generational wealth.

Mark Pinilla is a NAHREP 10 Certified Trainer for this exact reason. He helps individuals break old money patterns, make strategic financial decisions, and build lives based on equity, not appearance.

Once you understand how the game works, you stop playing small.

Five Steps to Redefine Wealth

Review your last 30 days of spending. What built your future and what fed your image?

Open a brokerage account. Start with what you have. Consistency beats size.

Replace your content diet. Follow educators, not flexers.

Talk about wealth at home. Normalize it.

Before every expense, ask: does this build freedom?

Redefine Wealth to Build Lasting Prosperity

This is more than a phrase. It’s a strategy.

To build lasting prosperity, Latinos must stop outsourcing wealth to appearance. The future belongs to those who invest, not impress.

Discipline #1 demands clarity and courage. Clarity to define what really matters. Courage to make decisions that honor that clarity.

Start small. Stay focused. Keep growing. The legacy you build will be louder than anything you wear.

Call to Action

If you’re ready to stop chasing appearances and start building real wealth, connect with someone who can guide you through the process.

Mark Pinilla is a Certified NAHREP Trainer who teaches Latino professionals and families how to shift from survival thinking to legacy creation. Through workshops, private coaching, and speaking events, he equips individuals with the mindset and tools needed to thrive financially.

To learn more or to book Mark for your next event, visit markpinilla.com or follow him on social media for ongoing education and inspiration.

Your financial breakthrough starts with better beliefs. Don’t wait. Take the first step toward building a life you don’t have to escape from.

What’s standing between you and your financial freedom? For many, it’s a three-digit number: your credit score. But the good news? You have the power to change it and boost your credit score.

Improving your credit score isn’t just about better loan terms or lower interest rates—it’s about building confidence and opening doors to new financial opportunities. Let’s explore how real strategies, smart decisions, and the right mindset can transform your financial path.

How Maria Turned Her Credit Around

Maria, a driven marketing professional, found herself stuck with a credit score of 620. The weight of a high credit card balance and a Home Equity Line of Credit (HELOC) was holding her back. Sound familiar?

Her Challenges:

High Credit Utilization: Credit cards nearing their limit were keeping her score low.

Complex Debt Mix: Managing both a credit card and a HELOC added financial strain.

What She Did:

Tackled Credit Card Debt First: Knowing that reducing credit utilization could quickly boost her score, Maria focused on paying down her credit cards.

Stayed Consistent with HELOC Payments: While the impact was slower, maintaining regular payments supported her long-term financial health.

Minimized Debt: Inspired by NAHREP’s Discipline #4, Maria committed to minimizing debt to build long-term financial stability. Discipline #4 states: “Minimize Debt because it is the biggest enemy to wealth.” This principle emphasizes the importance of avoiding unnecessary debt and focusing on paying down existing obligations. Maria prioritized reducing her debt load, understanding that lower debt levels meant less financial stress and better credit health. By adopting this discipline, she created more room for financial growth and resilience. (Learn more about NAHREP 10)

The Result?

Within six months, her credit score soared to 700.

Maria gained not just financial leverage but confidence in managing her money.

If Maria can do it, so can you.

5 Simple Steps to Boost Your Credit Score

Check Your Credit Report: Know where you stand. Identify errors or negative factors.

Cut Down Credit Card Balances: Keeping your utilization below 30% (or ideally 10%) can give your score a quick lift.

Stay Consistent with Payments: Never miss a due date—payment history makes up 35% of your credit score.

Mix Up Your Credit: Having a combination of credit types can improve your score over time.

Live Smart, Spend Smarter: Budget wisely. Building financial resilience now prepares you for the unexpected.

Want to Dive Deeper on boosting your credit score?

Check out “Your Score: An Insider’s Secrets to Understanding, Controlling, and Protecting Your Credit Score” by Anthony Davenport. It’s packed with strategies to help you navigate the credit system with confidence. Buy it on Amazon

Ready to Take Control of Your Financial Future?

Improving your credit score isn’t just a financial move—it’s a lifestyle shift. It’s about taking control, making intentional decisions, and setting yourself up for long-term success.

If you’re ready to boost your credit score and take charge of your financial journey, connect with Mark Pinilla for personalized guidance. His expertise can help you design a strategy that fits your goals and gets results.

What’s your biggest challenge with credit? Consistent effort, smart strategies, and expert advice can transform your credit and your financial future. Let’s take that first step together!

The Biggest Investing Mistake: Waiting for the Perfect Time

Many people delay investing because they believe they need a large sum of money or must wait for the “perfect time” to enter the market. The reality? Financial freedom isn’t about timing the market—it’s about time in the market. The earlier and more consistently you invest, the more wealth you build. Invest every month for financial freedom, and you’ll be amazed at the results over time.

One of the simplest and most effective strategies for wealth-building is Dollar Cost Averaging (DCA)—a method that helps you grow your investments steadily, avoid emotional decisions, and leverage the power of compounding interest.

What is Dollar Cost Averaging (DCA)?

Dollar Cost Averaging is an investment strategy where you invest a fixed amount of money at regular intervals—regardless of market conditions. This means you buy more shares when prices are low and fewer shares when prices are high, ultimately averaging out your purchase price over time.

Example of DCA in Action:

Imagine you invest $500 per month into a stock market index fund:

In a month when prices are high, your $500 buys fewer shares.

In a month when prices are low, your $500 buys more shares.

Over time, your cost per share averages out, reducing the risk of investing everything at a market peak.

Why DCA Works:

✅ Eliminates Emotional Investing – No need to worry about when to buy or sell. ✅ Reduces Market Timing Risks – You benefit from long-term market growth rather than short-term swings. ✅ Builds Wealth Consistently – Small, steady contributions grow significantly over time.

Automate Your Investments

The best way to stick with DCA is to automate your investments. Set up an automatic monthly transfer to an investment account, ensuring you stay consistent and take advantage of long-term growth. Invest every month for financial freedom, and let compounding do the rest.

The Power of Compounding Interest

Compounding interest is what turns small, consistent investments into massive wealth.

How It Works:

Your investments earn returns.

Those returns are reinvested, generating even more returns.

Over time, this cycle accelerates, creating exponential growth.

Example of Compounding Interest:

If you invest $1,000 at an 8% annual return:

After 1 year, you have $1,080.

After 2 years, you earn 8% on $1,080, growing to $1,166.

After 30 years, that $1,000 turns into $10,062—without adding a single extra dollar!

💡 Lesson: The earlier you start, the more powerful compounding becomes. Even small amounts invested today can lead to significant wealth.

The Rule of 72: How Your Money Doubles

The Rule of 72 is a simple formula to estimate how long it takes for your investment to double based on its return rate.

Formula:

72 ÷ Annual Interest Rate = Years to Double

Example:

If your investments earn an 8% return, your money doubles every 9 years (72 ÷ 8 = 9).

If you start with $10,000, in 9 years it becomes $20,000, then $40,000 in 18 years, then $80,000 in 27 years—without adding more money!

💡 The sooner you start, the more doubling cycles you get.

NAHREP Discipline #5: Invest at Least 20% of Your Income

The National Association of Hispanic Real Estate Professionals (NAHREP) created 10 disciplines for wealth-building, and Discipline #5 emphasizes investing at least 20% of your income in appreciating assets.

Why This Rule Matters:

✅ Creates Generational Wealth – Investing in real estate, stocks, and businesses ensures long-term financial security. ✅ Shields You from Inflation – Your money grows rather than losing value in a savings account. ✅ Builds Passive Income – Investing allows your money to work for you instead of you working for money.

Imagine looking back 10 years from now, knowing you started investing today. The key to financial success is not how much you invest, but how early and consistently you do it.

Your Next Steps:

✅ Start Now – Begin with any amount and stay consistent. ✅ Commit to Your Financial Future – Small monthly investments compound into significant wealth. ✅ Need Guidance? Contact Mark for expert direction on improving your financial future.

Are You Playing the Money Game to Win—or Just Trying to Survive?

Struggling with financial mistakes like poor money management, overspending, and lack of planning? This guide reveals the top financial mistakes keeping you broke and offers proven solutions to fix them, boosting your wealth-building journey with Mark Pinilla.

Most people don’t fail financially because they don’t work hard. They fail because they never learned the rules of the game. Money isn’t just about what you earn—it’s about how you manage, grow, and protect it.

The sad truth? Schools don’t teach financial literacy. Families don’t always pass down the right habits. And society tricks you into thinking success is about driving the newest car, wearing designer clothes, or living in the biggest house.

That’s why so many people struggle with financial mistakes. But here’s the good news: if you know what’s holding you back, you can fix it. And you don’t have to do it alone.

Let’s break down the three biggest financial mistakes people make—and how Mark Pinilla can help you break free and build real, lasting wealth.

1. Lack of Financial Literacy: What You Don’t Know CAN Hurt You

One of the most common financial mistakes is a lack of financial literacy.

They don’t know the difference between good debt and bad debt.

They think saving is enough—but inflation eats savings alive.

They believe working harder equals financial freedom—when it’s really about making money work for you.

The Solution: Learn from those who have mastered the game. Mark Pinilla is a mentor who simplifies wealth-building so you can take control of your future. His approach aligns with the NAHREP 10 Disciplines, ensuring you develop a real strategy, not just financial survival tactics.

2. Living Beyond Your Means: The Silent Wealth Killer

Another financial mistake is living beyond your means. People making six figures still drown in debt because their spending matches their income.

The upgraded house

The leased luxury car

The five-star vacations (paid on credit)

The Solution:Mark Pinilla teaches the discipline of living below your means (NAHREP Discipline #3)—not as a sacrifice, but as a strategy.

3. Failure to Plan for the Future: Hope Is Not a Strategy

Failing to plan for the future is a critical financial mistake.

No emergency fund? One unexpected expense can wipe you out.

No investments? You’ll work forever because your money isn’t working for you.

The Solution:Mark Pinilla helps shift from reactive to proactive wealth-building. As NAHREP’s Discipline #5 states, real estate and stocks are great ways to build wealth.

Take Action: Your Financial Freedom Starts Now

If you see yourself in any of these financial mistakes, don’t panic—take action.

At the young age of 20, Juan Sebastian Jimenez exemplifies the principles of the NAHREP 10 Disciplines, particularly Discipline #1: Have a Mature Understanding of Wealth and Prosperity. This principle teaches us that true wealth is not measured by material possessions but by long-term financial security and well-being. Sebas embodies this by making his money work for him, much like the “Investor” mindset from Rich Dad Poor Dad’s Cashflow Quadrant.

Financial Discipline: Sebas a Prodigy at Just 20 Years Old

Sebas graduated high school with strong foundations in financial literacy, wealth management, and personal finance success, earning an associate’s degree, earning a full scholarship to Florida International University. While managing full-time work as a Panda Express store manager, he trains to become a general manager, overseeing operations, staff, and financials — all before turning 21!

With some guidance, Sebas maximized his 401k contributions, opened a Roth IRA, and established a high-yield savings account — a shining example of Discipline 1 in action.

Discipline 3:Living below his means by keeping expenses low, preparing for economic downturns, and saving diligently with a high-yield money market account for emergencies and short-term goals.

Discipline 4:Meeting financial obligations with focus and discipline by minimizing debt and managing financial responsibilities carefully.

Discipline 5:Investing in the market through 401k and Roth IRA, emphasizing real estate and stocks as secure wealth-building strategies.

Discipline 8:Maintaining physical fitness through regular gym sessions, recognizing that health is as important as wealth.

Discipline 9:Demonstrating generosity through community service, giving time and resources to those less fortunate.

As a NAHREP 10 Certified Trainer, Mark Pinilla celebrates Sebas’ financial maturity, wishing he had the same wisdom at that age.

Want to build your financial future like Sebas and achieve financial discipline or build financial wealth? 👉 Contact Mark Pinilla today and start your journey to financial success.

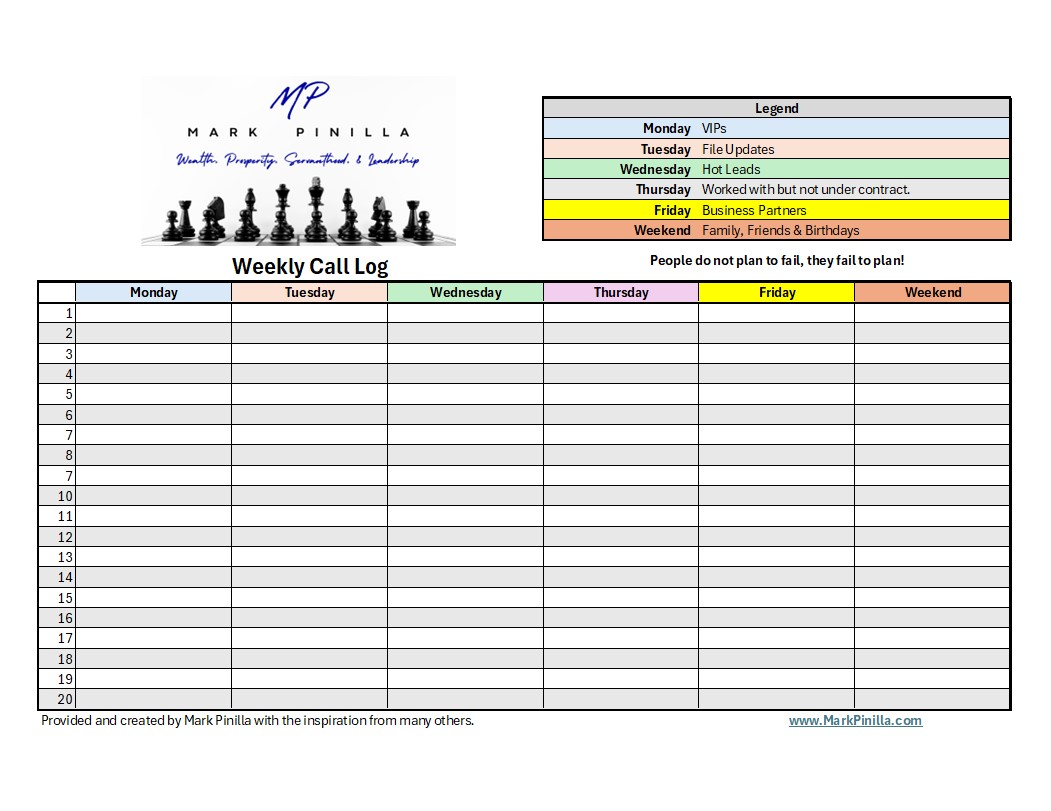

Success in business and life doesn’t happen by chance—it happens by planning. As Rick Guerrero, a NAHREP 10 Certified Trainer, emphasizes, preparation is everything. He starts each week by creating a call log every Sunday, setting the foundation for intentional and productive interactions. His approach mirrors NAHREP Discipline #2: Be in the top 10% of your profession by taking your craft seriously and working toward mastery. Learn more about the NAHREP 10 Disciplines here.

According to statistics, 70% of buyers and sellers choose a real estate agent based on referrals from friends and family. This underscores the importance of maintaining personal and professional connections. Planning calls with intention, as suggested by Rick and Sara, ensures you never miss an opportunity to nurture these relationships.

Real Estate Insights for Relationships

To add his personal touch to the call log, Mark Pinilla, a NAHREP 10 Certified Trainer, added the weekend column. Birthdays and family milestones aren’t just personal—they can be professional goldmines. Studies show that buyers and sellers often prefer working with someone they know and trust. By incorporating these touchpoints into your weekend calls, you position yourself as their go-to expert when the time comes.

Action Plan with Mark Pinilla

For those looking to maximize their wealth-building strategy, contact Mark Pinilla, a trusted resource for investment properties and real estate expertise. Waiting is not in your best interest—contact Mark here.