We hear it everywhere:

“You should start investing.” If you’re looking for a beginner investing strategy, this post walks you through each step.

But for most people, that’s like being told to bake a pineapple upside-down cake. It’s not impossible. It just feels overwhelming without a clear recipe.

If you’re a young adult, married, raising kids, or simply trying to manage your money better, this guide is for you.

Step One: Build a Safety Net First

Before you invest, protect yourself and your family.

Life Insurance

If something happens to you, life insurance replaces your income and protects the people who depend on you.

Emergency Fund

Save 3 to 6 months of essential expenses. This gives you breathing room when life throws curveballs like job loss, medical bills, or car repairs.

Once these are in place, you’re ready to move forward.

Step Two: Take the Free Money First

If your employer offers a 401(k) match, always take it.

This is guaranteed money.

| Employer Match | Immediate Return |

|---|---|

| 100% match (dollar for dollar) | 100% return |

| $0.50 cents per dollar | 50% return |

| $0.25 cents per dollar | 25% return |

Even at 25%, that’s more than double what financial planners expect from the market in a single year.

What Financial Planners Use for Forecasting

Planners use historical averages to estimate long-term growth. These are not guarantees, just benchmarks:

| Time Horizon | Estimated Annual Return |

| 20+ years | 8 to 10% |

| 10–20 years | 6 to 9% |

| 0–10 years | 3 to 7% (more volatile) |

This is why the employer match is so powerful. It gives you a return before your money even enters the market.

Step Three: Open an IRA

If you’ve maxed out your 401K match, or if your job doesn’t offer a plan, your next step is an IRA.

Traditional IRA

- Uses pre-tax money

- May reduce your taxable income

- Taxes are paid later in retirement

Good if you need tax relief now.

Roth IRA

- Uses after-tax money

- Grows tax-free

- Withdrawals in retirement are not taxed

Good if you expect higher taxes later or want tax-free income.

You can have both, but the total contribution across Traditional and Roth IRAs is capped each year.

Step Four: Consider Annuities (Optional)

If you’ve already maxed out your 401(k) and IRA, some people use annuities to invest more and defer taxes.

Annuities can offer:

- Tax-deferred growth

- Predictable income in retirement

- Lifetime payout options

However, they aren’t for everyone. Always talk with a licensed advisor before adding them to your plan.

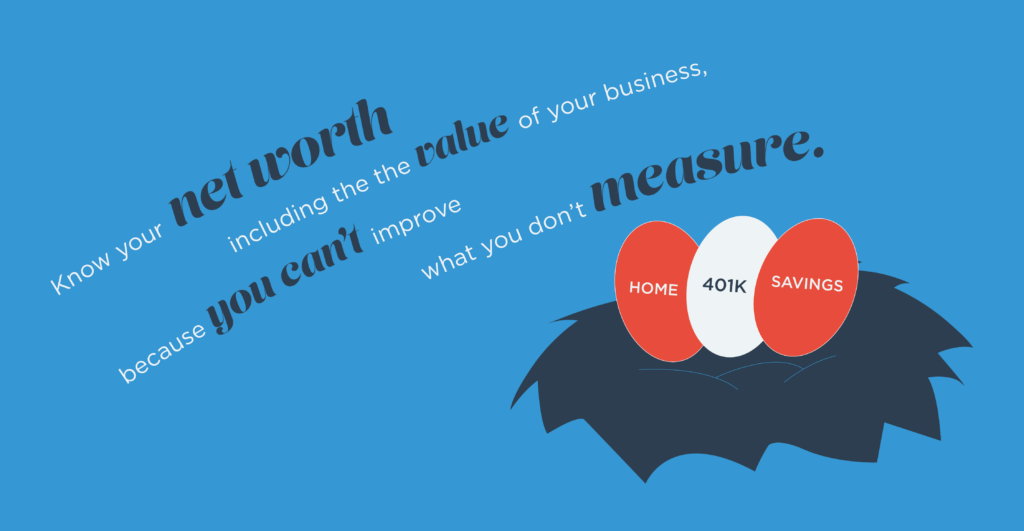

Step Five: Know Your FIN and Your Net Worth

Your FIN (Financial Independence Number) is the amount of money you need to retire comfortably without needing to work again.

This number gives you direction:

- How much you’ll need

- When you could reach it

- How much you should invest each month

But here’s the key:

You can’t improve what you don’t measure.

That’s why NAHREP 10 Discipline #6 says:

Know your net worth, including the value of your business.

This should be reviewed every year.

Your net worth is your scoreboard. Your FIN is your goal line. Reviewing both keeps your financial strategy focused, accurate, and relevant to your goals.

Ready to Build Your Strategy?

If you’re ready to stop guessing and start building a real plan, I can help.

📩 Schedule your strategy session:

🔗 www.markpinilla.com/contact

📱 Follow for tips and updates:

🌐 Google Business

📸 Instagram @markpinilla

💼 LinkedIn

You don’t need to be an expert.

You just need a clear plan and the right guide.

👉 Let’s connect now and take the first step toward your Financial Independence Number.