Most families do not have a money problem. They have a clarity problem. They work hard, they pay bills, they try to do the right things, but the plan is not written down. The numbers are not defined. The documents are not organized. Then life happens. A health scare. A job change. A death in the family. And the people you love end up trying to sort it out under stress.

This free Master Class is designed to change that. Mark will teach financial education in a way that is simple, direct, and focused on action. You will define what matters, calculate the key numbers that drive your future, and understand the protections that keep your family steady if life changes fast.

Mark will help you define:

-

Goals and dreams, what you want life to look like and why it matters

-

An approximate Financial Independence Number, the target that makes work optional

-

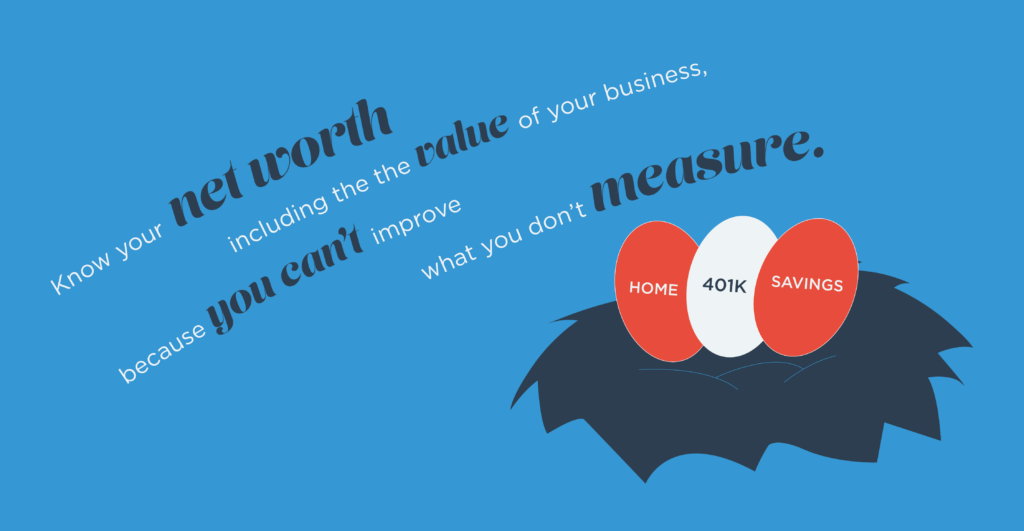

Net worth, what you own, what you owe, and what needs attention

-

Your 3 to 6 month emergency fund target, based on real monthly essentials

-

Family income protection, life insurance based on need and responsibilities

-

The need for asset protection, transfer of wealth, and living wills, so your family has direction and control

This class is for people who want peace of mind. People who want to build generational wealth with intention, not with guesswork. People who want their family protected, and their affairs organized, so loved ones are not left to figure out finances, decisions, and documents at the hardest possible time.

You will leave with clarity, a checklist, and your next steps. If you want help turning your results into a simple plan, you will have the option to sit down with Mark for a free Financial Needs Analysis.

Take this step for your future. Take it for your family. Let’s build your legacy together.